Budget 2026 Home Loan Deduction Limit: Rumour or Reality?

If you're planning to buy a house or already have a home loan, the next few days could change your financial equation dramatically. The buzz in tax and real estate circles is deafening: Will Budget 2026 increase the home loan interest deduction from ₹2 lakh to ₹5 lakh?

This isn't just another budget speculation-it's a potential game-changer that could put ₹90,000 extra cash in your pocket every year. Real estate agents are using this rumor to close deals, financial advisors are recalculating tax savings, and homebuyers are in a dilemma: Should I buy now or wait till February 1st?

Let me break down everything you need to know about this viral topic, backed by numbers, expert opinions, and practical advice.

The Current Reality: Why ₹2 Lakh Doesn't Cut It Anymore

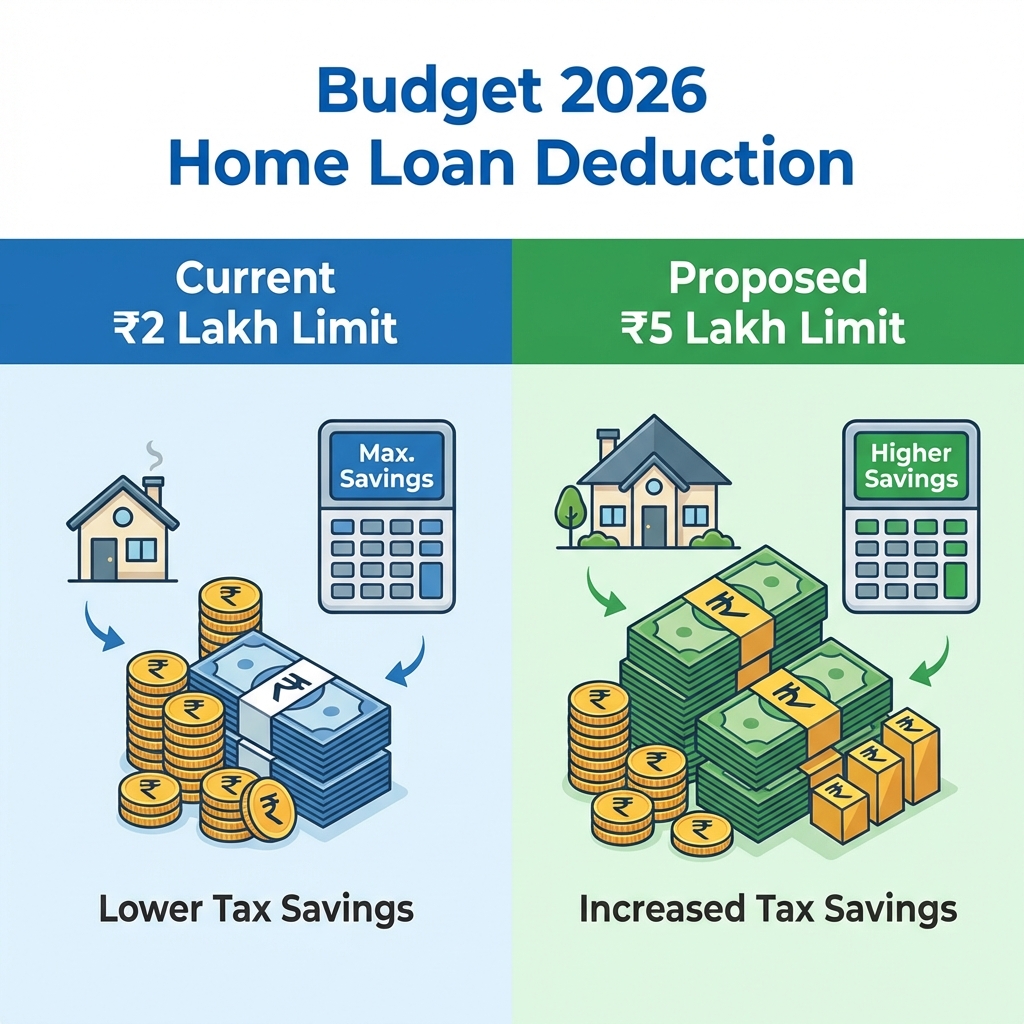

Under Section 24(b) of the Income Tax Act, if you have a home loan for a self-occupied property, you can claim a deduction of up to ₹2 lakh per year on the interest paid.

Sounds good? Not really. Here's why:

The Math That Doesn't Add Up

Let's take a typical home loan scenario in 2026:

- Property Value: ₹75 lakh (average 2BHK in Gurugram/Noida/Pune)

- Loan Amount: ₹60 lakh (80% LTV)

- Interest Rate: 9% (current market rate)

- Tenure: 20 years

- Annual Interest (Year 1): Approximately ₹5.3 lakh

Tax Benefits on Home Loan FY 2026-27: The Current Scenario

If you're in the 30% tax bracket (income above ₹15 lakh):

- Maximum Deduction: ₹2,00,000

- Tax Saved: ₹2,00,000 × 30% = ₹60,000 per year

The Rumor: Section 24(b) Limit Increase 2026

According to reports from Upstox and statements from industry bodies like CREDAI and NAREDCO, there's a strong demand to increase the Section 24(b) limit to ₹5 lakh.

Why Experts Are Demanding This Change

1. Inflation Adjustment: The ₹2 lakh limit was set years ago when property prices were 40-50% lower 2. Affordable Housing Push: The government wants to boost affordable housing-this is a direct incentive 3. Interest Rate Reality: With rates at 8.5-9.5%, even a ₹40 lakh loan generates ₹3+ lakh annual interest 4. Economic Stimulus: More tax savings = more disposable income = higher consumption

What Financial Experts Are Saying

Tax consultancies and real estate analysts have been vocal:

- "The ₹2 lakh limit is outdated and needs immediate revision to ₹5 lakh" - Industry experts

- "This move could revive the stagnant mid-income housing segment" - Real estate analysts

- "It's a win-win: taxpayers save more, real estate gets a boost" - Economic commentators

The Calculation That's Going Viral

Here's the comparison that's making rounds on social media and WhatsApp groups:

Current vs Proposed: The Money You'll Save

| Parameter | Current (₹2L Limit) | Proposed (₹5L Limit) | Difference | |--------------|------------------------|-------------------------|----------------| | Maximum Deduction | ₹2,00,000 | ₹5,00,000 | +₹3,00,000 | | Tax Saved (30% bracket) | ₹60,000 | ₹1,50,000 | +₹90,000 | | Tax Saved (20% bracket) | ₹40,000 | ₹1,00,000 | +₹60,000 | | Tax Saved (10% bracket) | ₹20,000 | ₹50,000 | +₹30,000 |

Real-World Impact

Let's say you're a software engineer earning ₹18 lakh per year with a ₹60 lakh home loan:

Current Scenario:

- Annual interest paid: ₹5,20,000

- Deduction claimed: ₹2,00,000

- Tax saved: ₹60,000

- Effective interest cost: ₹4,60,000

- Annual interest paid: ₹5,20,000

- Deduction claimed: ₹5,00,000 (can't exceed actual interest)

- Tax saved: ₹1,50,000

- Effective interest cost: ₹3,70,000

Over a 20-year loan tenure, that's ₹18 lakh in extra savings (not accounting for reducing interest over time).

Real Estate Impact of Union Budget 2026

If this deduction limit increases, here's what happens to the real estate market:

1. Immediate Demand Spike

Property in the ₹50-80 lakh range becomes significantly more affordable on a post-tax basis. Expect:

- 10-15% increase in inquiries within weeks of the announcement

- Faster closures as fence-sitters jump in

- Developer confidence leading to new launches

2. Will Property Prices Rise After Budget 2026?

Short answer: Likely, yes.

Here's the logic:

- Increased affordability = Higher demand

- Higher demand + Limited supply (especially in metros) = Price increase

- Developers will factor in the tax benefit and adjust pricing accordingly

3. Best Markets to Watch

If the ₹5 lakh limit passes, these markets will see maximum action:

- Gurugram (Golf Course Extension, Dwarka Expressway, Sohna Road)

- Noida/Greater Noida (Expressway projects)

- Pune (Hinjewadi, Baner, Wakad)

- Bengaluru (Whitefield, Electronic City)

- Mumbai MMR (Thane, Navi Mumbai)

The Dilemma: Should You Buy Before February 1st?

This is the million-rupee question. Let me give you both sides:

Case FOR Buying Now (Before Budget)

1. Price Protection: If the announcement is positive, prices will jump. Lock in today's rates. 2. Inventory Advantage: Best units get sold first. Don't lose out on your preferred floor/facing. 3. Negotiation Power: Developers are currently offering discounts to close Q4 sales. Post-budget, that leverage disappears. 4. Interest Rate Risk: RBI might cut rates if budget is expansionary, but property prices will rise faster than rate cuts help.

Case FOR Waiting (Till After Budget)

1. Confirmation: What if the limit doesn't increase? You've committed without the tax benefit. 2. Better Deals: If the announcement is negative or neutral, developers might panic and offer steeper discounts. 3. Clarity on Other Sops: Budget might announce other schemes (interest subvention, stamp duty relief) that could be better.

My Professional Advice

As a CA who's advised hundreds of homebuyers, here's my take:

Buy now if:

- You've found the right property at the right price

- You're buying for self-use, not speculation

- You can afford the EMI comfortably even without the extra tax benefit

- The property is in a high-demand micro-market

- You're purely speculating on the tax benefit

- You're stretching your finances to afford the EMI

- The property is in an oversupplied market with weak fundamentals

Other Budget 2026 Expectations for Homebuyers

Beyond Section 24(b), here are other demands from the real estate sector:

1. Principal Repayment Deduction (Section 80C)

Currently capped at ₹1.5 lakh (combined with other 80C investments). Demand: Separate ₹2 lakh limit for home loan principal.

2. Stamp Duty Rationalization

Stamp duty varies wildly across states (4% to 7%). Demand: Uniform 3% across India to reduce transaction costs.

3. Affordable Housing Definition

Current ceiling: ₹45 lakh. Demand: Increase to ₹75 lakh to reflect market realities in metros.

4. GST on Under-Construction Properties

Current: 5% (with ITC) or 1% (without ITC). Demand: Reduce to 1% uniformly or exempt affordable housing.

Tax Planning Strategy for FY 2026-27

Regardless of what Budget 2026 brings, here's how to optimize your home loan tax benefits:

1. Choose the Right Tax Regime

The Old Tax Regime allows Section 24(b) deduction. The New Tax Regime doesn't.

If you have a large home loan, the Old Regime will likely save you more tax-even if the New Regime has lower slab rates.

2. Co-Ownership Strategy

If you buy property jointly with your spouse:

- Each co-owner can claim ₹2 lakh deduction (current limit)

- Total household benefit: ₹4 lakh deduction = ₹1.2 lakh tax saved (at 30% bracket)

3. Pre-Construction Interest

Interest paid during construction can be claimed in 5 equal installments after possession. Don't forget to claim this!

4. Let-Out Property Advantage

If you rent out your second property, there's no ₹2 lakh cap on interest deduction. You can claim the entire interest amount against rental income.

What If the Limit Doesn't Increase?

Let's be realistic: Budget announcements are unpredictable. What if February 1st comes and goes without any change to Section 24(b)?

Don't Panic

1. The ₹2 lakh benefit still exists: It's not going away 2. Principal repayment under 80C still gives you up to ₹1.5 lakh deduction 3. Long-term appreciation: Real estate in good locations appreciates 6-8% annually, far exceeding the tax benefit

Alternative Tax-Saving Strategies

If the home loan benefit doesn't increase, maximize other deductions:

- NPS (80CCD(1B)): Additional ₹50,000 deduction

- Health Insurance (80D): Up to ₹25,000 (₹50,000 for senior citizens)

- Education Loan Interest (80E): No upper limit

- Donations (80G): 50-100% deduction depending on the institution

The Bigger Picture: Budget 2026 and Real Estate

This potential change to Section 24(b) is part of a larger government strategy:

1. Housing for All

The government's mission to provide affordable housing to every Indian by 2030 requires demand-side incentives. Tax benefits are the easiest lever.

2. Economic Stimulus

Real estate is a massive employment generator (construction, materials, services). Boosting this sector has multiplier effects on GDP.

3. Formalizing the Economy

Higher tax benefits encourage people to take formal home loans (instead of cash deals), bringing more transactions into the tax net.

Key Takeaways

1. The Rumor is Real: There's genuine demand from industry bodies to increase Section 24(b) limit to ₹5 lakh 2. The Math is Compelling: ₹90,000 extra annual savings for 30% bracket taxpayers 3. Real Estate Will React: Positive announcement = price spike in mid-income housing 4. Don't Speculate: Buy property based on fundamentals, not tax rumors 5. Plan for Both Scenarios: Optimize your tax planning whether the limit increases or not

Final Thoughts

As we count down to February 1st, the anticipation is palpable. Will the Finance Minister deliver the ₹5 lakh home loan deduction that millions of homebuyers are hoping for?

Honestly, I'd give it a 60-40 chance in favor. The government has shown willingness to support real estate (PMAY, interest subvention schemes), and this move aligns with their affordable housing mission. But fiscal constraints are real, and every tax benefit has a revenue cost.

My advice: Don't let budget speculation paralyze you. If you've found the right property at the right price, go for it. The tax benefit-whether ₹2 lakh or ₹5 lakh-is the cherry on top, not the cake itself.

And if you're already a homeowner with a running loan, keep your fingers crossed. An extra ₹90,000 in your pocket every year would be a very welcome gift!

---*Disclaimer: This article analyzes budget expectations and market speculation. Tax laws are subject to change based on the Finance Bill 2026. For personalized tax planning and home loan optimization strategies, consult CA Atul Mangal & Co.*

Related Reading: